Previous Session Recap

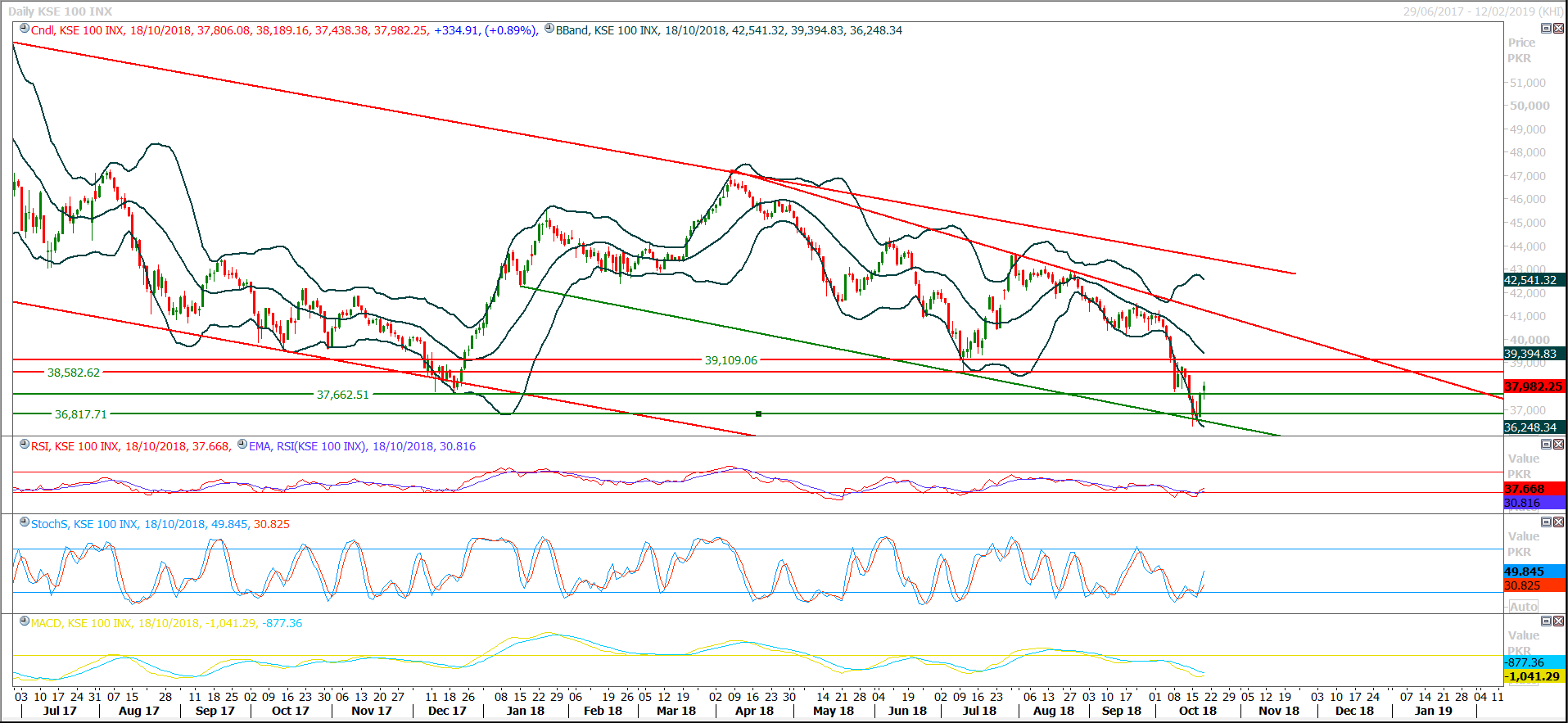

Trading volume at PSX floor increased by 29.23 million shares or 15.06% on DoD basis, whereas the Benchmark KSE100 index opened at 37,806.08, posted a day high of 38,189.16 and day low of 37,438.38 points while the session suspended at 37,982.25 with net change of 334.91 points and net trading volume of 115.14 million shares. Daily trading volume of KSE100 listed companies increased by 15.14 million shares or 14.94% on DoD basis.

Foreign Investors remained in net selling position of 3.89 million shares and net value of Foreign Inflow dropped by 1.92 million US Dollars. Categorically, Foreign Individuals, Corporate and Overseas Pakistanis investors remained in net selling positions of 0.02, 2.95 and 0.91 million shares. While on the other side Local Individuals, Banks and NBFCs remained in net selling positions of 0.55, 1.06 and 2.21 million shares but Local Companies, Mutual Fund, Brokers and Insurance Companies remained in net buying positions of 0.28, 4.29, 0.88 and 1.98 million shares respectively.

Analytical Review

Wall St. slides as Saudi Arabia, Italy add to economic concerns

U.S. stocks fell more than 1 percent on Thursday as the European Commission issued a warning regarding Italy’s budget and concerns mounted over the possibility of strained relations between the United States and Saudi Arabia, further denting investors’ appetite for risk amid global trade tensions and rising interest rates. The benchmark S&P 500 index closed just above its 200-day moving average, a key indicator of long-term price trends. S&P 500 technology and consumer discretionary stocks fell more than 2 percent, as did the tech-heavy Nasdaq. Among the S&P’s major sectors, only utilities and real estate, considered defensive, avoided losses.

Tractor manufacturers’ refunds mount to over Rs5b

Pakistan Automotive Manufacturers Association director general Abdul Waheed Khan has drawn the attention of Federal Finance Minister Asad Umar towards huge refunds of tractor manufacturers held back by the FBR since April 2018, mounting to over Rs.5 billion. In a letter written to Asad Umar, he said that this huge amount has created a liquidity crunch among the tractor companies. The root cause of this continuous accrual of sales tax refunds is an anomaly that sales tax of 17 percent is being charged on imported tractor parts at import stage, which always results in refunds later as sales tax on tractors is 5 percent, thus creating huge financial issue.

IMF programme positive for Pakistan: Moody's

The Moody’s has said that International Monetary Fund (IMF) programme would not only bridge the financing gap for Pakistan but also serve as a strong signal to other creditors to meet financing requirements over the coming years. The International rating agency, Moody’s has estimated Pakistan’s gross external financing needs for fiscal 2019 to be around $30 billion, of which $7-$8 billion are the government’s external repayments. The financing gap – which excludes foreign-exchange reserves – is likely to total $8-$9 billion; taking into account the government’s borrowing plans and our expectations for capital inflows including foreign direct investment and portfolio flows.

FDI dips 42pc as Chinese investment declines

Foreign direct investment (FDI) declined by 42 per cent during the first quarter of current fiscal year compared to the same period last year falling short of even half billion mark. Central bank’s data revealed that FDI during July-September FY19 clocked in at $439.5 million compared to $765m last year. Pakistan desperately requires foreign exchange inflows to cap the rising current account deficit. The decline in inflows comes at a time when Pakistan’s depleting foreign exchange reserves have already fallen to alarmingly low levels at $14.6 billion including State Bank of Pakistan’s (SBP) $8.089bn providing enough only for two months of import cover.

LSM shrinks 3.33pc in August

The large-scale manufacturing (LSM) index entered negative growth of 3.33 per cent year-on-year in August, data shared by the Pakistan Bureau of Statistics revealed on Thursday. The decline in big industrial production in August has caused fears that economic growth in the country may slow down. July posted a meagre increase of 0.5pc YoY. In 2017-18, the LSM posted a growth of 5.4pc YoY by missing the target of 6.3pc. Between July-August, the growth dropped 1.17pc YoY.

U.S. stocks fell more than 1 percent on Thursday as the European Commission issued a warning regarding Italy’s budget and concerns mounted over the possibility of strained relations between the United States and Saudi Arabia, further denting investors’ appetite for risk amid global trade tensions and rising interest rates. The benchmark S&P 500 index closed just above its 200-day moving average, a key indicator of long-term price trends. S&P 500 technology and consumer discretionary stocks fell more than 2 percent, as did the tech-heavy Nasdaq. Among the S&P’s major sectors, only utilities and real estate, considered defensive, avoided losses.

Pakistan Automotive Manufacturers Association director general Abdul Waheed Khan has drawn the attention of Federal Finance Minister Asad Umar towards huge refunds of tractor manufacturers held back by the FBR since April 2018, mounting to over Rs.5 billion. In a letter written to Asad Umar, he said that this huge amount has created a liquidity crunch among the tractor companies. The root cause of this continuous accrual of sales tax refunds is an anomaly that sales tax of 17 percent is being charged on imported tractor parts at import stage, which always results in refunds later as sales tax on tractors is 5 percent, thus creating huge financial issue.

The Moody’s has said that International Monetary Fund (IMF) programme would not only bridge the financing gap for Pakistan but also serve as a strong signal to other creditors to meet financing requirements over the coming years. The International rating agency, Moody’s has estimated Pakistan’s gross external financing needs for fiscal 2019 to be around $30 billion, of which $7-$8 billion are the government’s external repayments. The financing gap – which excludes foreign-exchange reserves – is likely to total $8-$9 billion; taking into account the government’s borrowing plans and our expectations for capital inflows including foreign direct investment and portfolio flows.

Foreign direct investment (FDI) declined by 42 per cent during the first quarter of current fiscal year compared to the same period last year falling short of even half billion mark. Central bank’s data revealed that FDI during July-September FY19 clocked in at $439.5 million compared to $765m last year. Pakistan desperately requires foreign exchange inflows to cap the rising current account deficit. The decline in inflows comes at a time when Pakistan’s depleting foreign exchange reserves have already fallen to alarmingly low levels at $14.6 billion including State Bank of Pakistan’s (SBP) $8.089bn providing enough only for two months of import cover.

The large-scale manufacturing (LSM) index entered negative growth of 3.33 per cent year-on-year in August, data shared by the Pakistan Bureau of Statistics revealed on Thursday. The decline in big industrial production in August has caused fears that economic growth in the country may slow down. July posted a meagre increase of 0.5pc YoY. In 2017-18, the LSM posted a growth of 5.4pc YoY by missing the target of 6.3pc. Between July-August, the growth dropped 1.17pc YoY.

Market is expected to remain volatile therefore its recommended to stay cautious while trading during current trading session.

Technical Analysis

The Benchmark KSE100 Index have continued its bullish journey after generating a morning star on daily chart and have tried to hit 38% correction of its last bearish rally during last trading session. Daily momentum indicators have generated bullish crossovers while weekly and hourly momentum indicators are trying to follow this trend. As of now index have major resistances ahead at 38,580 and 38,900 points because these both regions fall on a strong horizontal resistant region and 50% correction of latest bearish rally. Previously these both regions have resisted against bearish momentum therefore it’s expected that now these would try to provide resistance against current pull back. While on flipside index have supportive regions standing at 37,600 and 36,800 points. It’s recommended to stay cautious while trading during current trading session because if index would not succeed in closing 38,300 or 38,580 points during current trading session then current bullish sentiment would start expiring.

Script wise trading could be beneficial during current trading session instead of following index sentiment because some market leader scripts are trading near to their resistant regions and buying after penetration of these regions or buying on dip with strict stop loss of their supportive region could be very beneficial. TRG would try to maintain its bullish momentum towards 24.23 and if it would succeed in closing above 24.50 in coming days then next target would be 25.60. If PSO would succeed in penetration of 232 on hourly closing basis then it can target 237 and 241 while PAEL would target 27.50 and 28 in coming days if it would succeed in closing above 24.80 during current trading session. DGKC and MLCF have resistant regions ahead and if these would succeed in penetration of 85.50 and 39.30 on hourly closing basis then these both would try to target 87 or 89 and 41 respectively.ISL is heading towards 70 and 67 Rs from where a pullback would be witnessed.

Script wise trading could be beneficial during current trading session instead of following index sentiment because some market leader scripts are trading near to their resistant regions and buying after penetration of these regions or buying on dip with strict stop loss of their supportive region could be very beneficial. TRG would try to maintain its bullish momentum towards 24.23 and if it would succeed in closing above 24.50 in coming days then next target would be 25.60. If PSO would succeed in penetration of 232 on hourly closing basis then it can target 237 and 241 while PAEL would target 27.50 and 28 in coming days if it would succeed in closing above 24.80 during current trading session. DGKC and MLCF have resistant regions ahead and if these would succeed in penetration of 85.50 and 39.30 on hourly closing basis then these both would try to target 87 or 89 and 41 respectively.ISL is heading towards 70 and 67 Rs from where a pullback would be witnessed.

To Open picture in original resolution right click image and then click open image in a new tab

To Open picture in original resolution right click image and then click open image in a new tab

0 Comments

No comments yet. Be the first to comment!

Please log in to leave a comment.